GST on Rent in 2025: Residential & Commercial Property Tax Rates

CA Vishal Agarwal

CA Vishal Agarwal is a highly skilled and dedicated Chartered Accountant with extensive expertise in Goods and Services Tax (GST). With years of experience in the field, he has established himself as a trusted advisor to businesses and individuals across multiple locations in Bihar. His deep understanding of GST regulations, compliance, and advisory services has helped numerous clients navigate the complexities of taxation with ease and confidence.

GST on rent has significant tax implications for both property owners and tenants renting real estate in India. While commercial properties and residential spaces leased to enterprises are subject to 18% GST, residential properties rented for personal use are exempt from GST. Landlords earning more than ₹20 lakh per year must register for GST and comply with tax laws.

GST is applicable to commercial property rentals, and companies can reduce their tax liability by claiming input tax credits (ITCs). The applicability of GST to co-working spaces, government leases, and educational institutions is governed by special provisions. Additionally, under the reverse charge mechanism (RCM), tenants renting residential space for business purposes are liable to pay GST. This blog will discuss the legal requirements for landlords to maintain compliance, when GST applies to rental income, and how ITC benefits companies that rent out commercial real estate.

Application of GST to Rental Income

Both landlords and tenants must understand the conditions under which GST applies to rental income. While not all rental transactions are subject to GST, certain conditions necessitate tax payment. The type of property (residential or commercial) and the tenant determine whether GST applies. Furthermore, whether the property is leased to an individual or a business organization, along with the landlord’s total rental revenue, affects GST liability.

GST on the Rent of Residential Property

GST does not apply to all residential property rentals. Regardless of the landlord’s overall rental income, residential properties rented for personal use are exempt from GST. However, the transaction is subject to 18% GST if a residential property is leased to a corporation or registered enterprise.

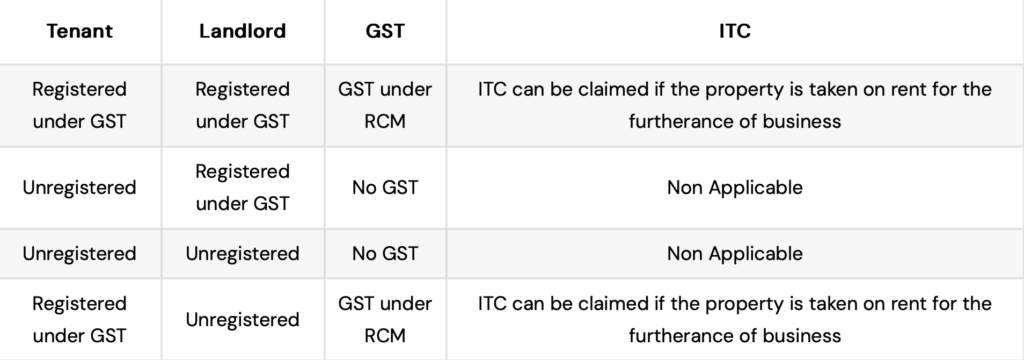

The reverse charge mechanism (RCM) is one of the distinctive features of residential property leasing. In this case, if the tenant is a registered business, they are responsible for paying GST instead of the landlord. In some cases, landlords are not required to collect or remit GST. However, the tax paid under RCM is a direct expense for the tenant and cannot be claimed as an Input Tax Credit (ITC). Businesses using rented residential areas for staff housing or guest accommodations are significantly affected by this legislation.

GST on Rent for Commercial Real Estate

Regardless of the tenant type, commercial property leases are always subject to 18% GST, unlike residential rentals. This implies that GST must be included on the rental invoice regardless of whether a business is renting an office building, store, warehouse, or commercial complex.

The landlord must collect 18% GST on rent and deposit it with the government if they are GST-registered. In certain situations, the tenant—rather than the landlord—may be obligated to pay GST under RCM if they are a registered business. This system streamlines the collection of commercial lease taxes while ensuring compliance.

When Is Rent Subject to GST?

If the total annual rental income exceeds ₹20 lakh (₹10 lakh in special category states), GST is applied to the rental revenue. All rental revenue from the same PAN is included in this criterion. The landlord must register for GST and impose tax on eligible rents if their total income exceeds this threshold.

Different rental agreements are subject to different GST treatments. While residential premises rented out for personal use are completely exempt from GST, the reverse charge mechanism (RCM) imposes 18% GST on residential unit leases to registered commercial entities. On the other hand, commercial property rentals are always subject to 18% GST; therefore, landlords must be aware of their tax responsibilities before leasing a space.

Landlord GST Registration

When your total rental income surpasses ₹20 lakh per year (₹10 lakh in states that fall under specific categories), you must register for GST if you are renting out your property. This holds true whether you rent home space to a business organization or lease commercial property.

Who Must Register for GST?

GST registration might be required if you rent out properties. Determining eligibility depends on several factors, including the property type, tenant category, and income threshold.

Who must register for GST on rental income is as follows:

- Landlords receive more than ₹20 lakh in rent (₹10 lakh in certain states).

- Owners who lease commercial real estate, regardless of the type of tenant.

- Residential landlords who lease properties to businesses (18% GST applies under RCM).

How Can a Landlord Register for GST?

As a landlord, you can ensure compliance and facilitate accurate tax filing by registering for GST. Key documents must be submitted via the GST portal, and the procedure is straightforward.

To facilitate a smooth registration process, follow these steps:

- Create an account by visiting the GST portal (www.gst.gov.in).

- Provide property details and proof of rental income on Form GST REG-01.

- Upload the required documents (bank account details, rent agreement, Aadhaar, and PAN).

- Upon approval, obtain your GSTIN (GST Identification Number).

Filing GST Returns on Rental Income

Landlords are required to submit GST returns following registration:

a. Rental invoicing on a monthly or quarterly basis (GSTR-1).

b. GSTR-3B: Tax liability summary return.

Failure to register or file returns may result in penalties and legal issues. Maintaining GST compliance avoids tax conflicts and guarantees a seamless renting experience.

Exemption from GST Payment

There are some situations where paying GST on rent is not required, such as:

- Renting a residential property for residential purposes: As previously stated, provided that neither party is GST-registered.

- Annual rental income under Rs. 20 lakh: The landlord is exempt from GST and is not required to pay tax on rent if the total annual rental income from all properties is less than Rs. 20 lakh (approximately $24,000).

- Specific property types: GST exemption also applies to rentals by charitable organizations, places of worship, and agricultural land.

Rental Property Input Tax Credit (ITC)

Companies that lease commercial real estate may reduce their tax liability by claiming the input tax credit (ITC) on GST paid on rent. Commercial leases are more economical because the 18% GST on rent can be deducted from the company’s output tax.

However, even if a company rents a home for its employees, ITC is not applicable to residential property rentals. The GST law limits ITC claims by treating residential property rent as an exempt supply.

Businesses that want to claim ITC on commercial rent must:

a. Ensure that the landlord provides accurate GST invoices.

b. Accurately report rent-related ITC in GSTR-1 and GSTR-3B.

c. To avoid ITC rejection or fines, steer clear of mismatches.

Businesses can lower their tax expenses by complying with GST regulations, and landlords should maintain clear tax records to prevent disputes.

Household Living Residential Rental

A landlord leasing a residential property (home, apartment, etc.) to a tenant for use as their primary residence is referred to as ‘residential dwelling rental. In most cases, this type of lease agreement is exempt from taxes such as India’s Goods and Services Tax (GST).

The following are important facts regarding renting a residential home for residential purposes:

Tax Repercussions

Exemption: As long as the renter is not registered for GST, renting a residential property in India for domestic use is typically exempt from GST. This indicates that the rent amount is not subject to tax.

Reverse Charge Mechanism (RCM): Under the RCM, the tax burden passes to the tenant if they are registered for GST. This implies that the tenant must pay GST at a rate of 18% on the rent. However, this law has some exceptions, such as when a tenant leases the property for personal residence rather than business use.

Local variations: It is important to note that tax laws vary by region in India. To find out the precise laws and regulations in your area, always consult a tax professional or the local tax authorities.

Terms of the Agreement

Lease agreement: The terms and circumstances of the rental, such as the rent amount, lease period, security deposit, maintenance obligations, and termination provisions, are usually outlined in a conventional lease agreement.

Utilities: Depending on the terms of the lease, utilities like waste disposal, power, and water may be paid for by the landlord or the renter.

Maintenance and repairs: The agreement should outline who is in charge of the property’s upkeep and repairs.

Conclusion

The new GST regulations on residential and commercial rent aim to simplify taxation and enhance transparency in real estate transactions. To avoid fines and ensure compliance, landlords and tenants must be aware of their GST obligations and eligibility for input tax credits.

Disclaimer

The content published on this blog is for informational purposes only. The opinions expressed here are solely those of the respective authors and do not necessarily reflect the views of Fintrac Advisors. We make no warranties regarding the completeness, reliability, or accuracy of this information. Any action you take based on the information presented on this blog is strictly at your own risk, and we will not be liable for any losses and damages in connection with its use. We recommend seeking professional expertise for any such work. External links on our blog may direct users to third-party sites beyond our control. We do not take responsibility for their nature, content, or availability.